Learn about the four ways a Unison Equity Sharing Agreement can end, including selling your home or choosing a buyout.

Cash-out refinancing can be a good option for homeowners who need quick access to funds, but it's not the right move for everyone. Fortunately, there are other options available to you.

If you want to tap into the equity built up in your home, home equity loans and home equity lines of credit (HELOCs) are two of the most popular, widely-known options available. You’ve probably also wondered, what exactly are the differences between them?

You’ve probably heard of home equity loans, and have a general idea of what they are. But if you’re looking for a way to access your growing home equity and considering your options, a “general idea” isn’t going to cut it.

It’s no secret that Americans are sitting on an enormous amount of home equity (nearly $30 trillion!) But sitting is a passive act; you may be wondering whether there’s a way you could make your equity actively work for you.

A cash-out refinance is a mortgage refinancing solution that allows homeowners to replace their existing mortgage with a new one–usually at a higher loan amount–and receive the difference between the two loans in cash.

You’ve probably heard it’s good to build equity in your home. But what is home equity, exactly? How can you calculate the equity you have in your home? What can you even use that home equity to do?

The "Zestimate" is a bit of a secret sauce, which Zillow will admit is not always perfect. But it's a valuable tool nonetheless – here's what we know about the calculation process.

If you're planning on putting less than 20% down, you'll likely need to anticipate paying for PMI. But how much of a burden is it? Read this article for some of the common amounts to expect.

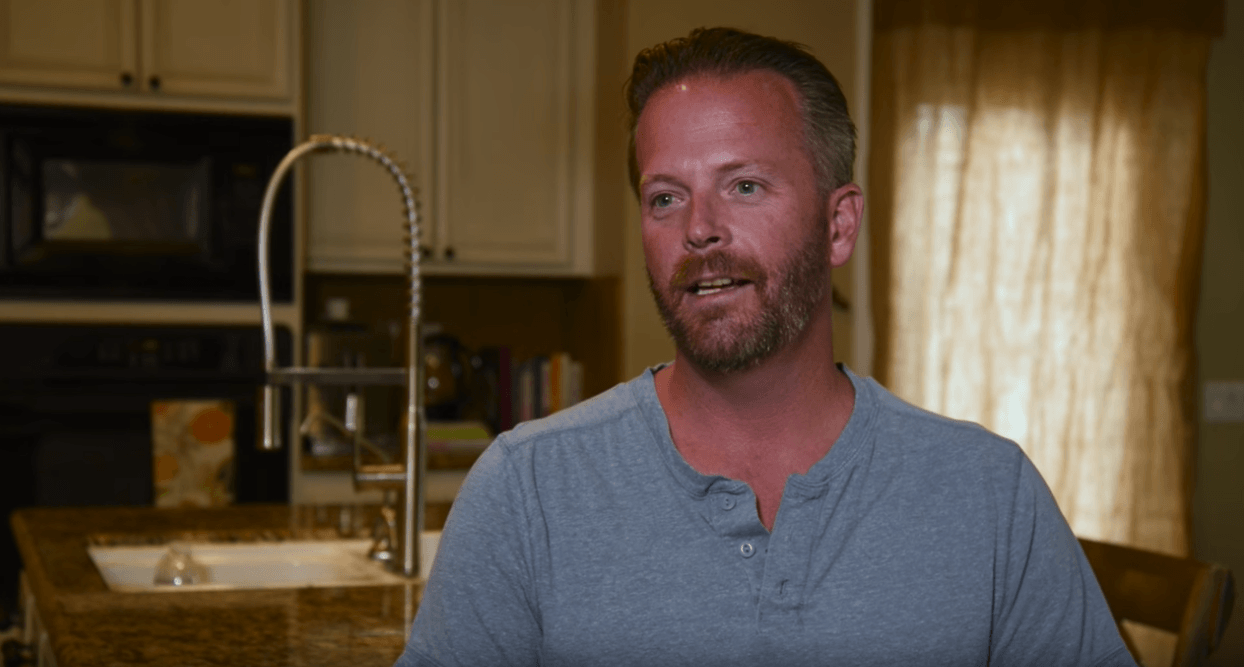

Leslie and John weren't sure about their next move – between debt, renovations, and bills. With a home equity sharing agreement from Unison, they didn't have to choose.

Unison helped this homeowner pay off debt and remodel their home with home equity funds.

It's easy to focus on the list price of a home, while ignoring the amount of interest that will likely accrue over the lifespan of your mortgage. Here's how to manage it and stay prepared.

PMI adds an additional monthly payment to your budget, but you may be able to avoid it completely. Read on for the easiest ways to reduce or remove the need for PMI entirely.

.png)